Money Management

Budgeting or Cash Flow Management: Which is Right For You?

Dec 2, 2021 12 min read

SUMMARY

- Budgeting is when you manage your income and expenditures over the course of a month.

- Cash flow management is when you track your income and expenses day-by-day to avoid temporary negative balances in your checking account.

- Cash flow management can help you avoid bank overdraft fees and keep tighter control over your day-to-day spending.

Looking to get a better handle on your month-to-month finances? When it comes to creating a plan for your money, you might assume a traditional budget is the only way to go. But it’s not the only money-management option out there, nor is it the ideal approach for everyone.

If you have an irregular income, unpredictable expenses, living paycheck-to-paycheck, or just want more control over your finances, you may want to consider an alternative to traditional budgeting: cash flow management.

So, what is cash flow management and how does it differ from traditional budgeting? More importantly, how do you determine which option is right for you? Let’s dig into the two methods to learn more.

But first, an interesting scenario.

Consider two people who each make $2000 per month and have $2000 in monthly expenses. They both spend their money exactly the same way, but at the end of the month, one of them ends up overspending by $70. How is that possible?

When the over-spender investigated the problem, they found that they spent $70 on bank overdraft fees. On a monthly basis, that person had enough income to cover their expenses, but bills came in at times when their bank account was dry.

Budgeting is a powerful tool for getting control of personal finances, but it doesn’t seem to work for everyone. Some have fluctuating incomes or expenses that are hard to predict. Others find that the timing of their expenses don’t line up with the timing of their income, like our scenario above. Maybe you’ve tried budgeting and felt that it never worked. If that is the case, you might want to try focusing on cash flow management instead of budgeting.

What Is traditional budgeting?

Traditional budgeting is the process of creating a detailed plan for your money based on your income and expenses. A successful budget can help ensure you have enough money each month for all your needs, some of your wants, your savings and any debts you’re repaying.

Although every budgeting scenario is unique, traditional budgets tend to work best for people who earn a steady, predictable income that exceeds their monthly expenses. Budgets can fall apart when expenses are difficult to categorize or predict. If your income is roughly the same each month and you regularly have enough money to cover your fixed and variable expenses, you’re likely a good candidate for budgeting.

How does traditional budgeting work?

From the 50/30/20 plan to “pay yourself first,” there are many different budgeting methods to choose from. However, the fundamental goal is always the same—to cover all your essential expenses and still have some money left over each month.

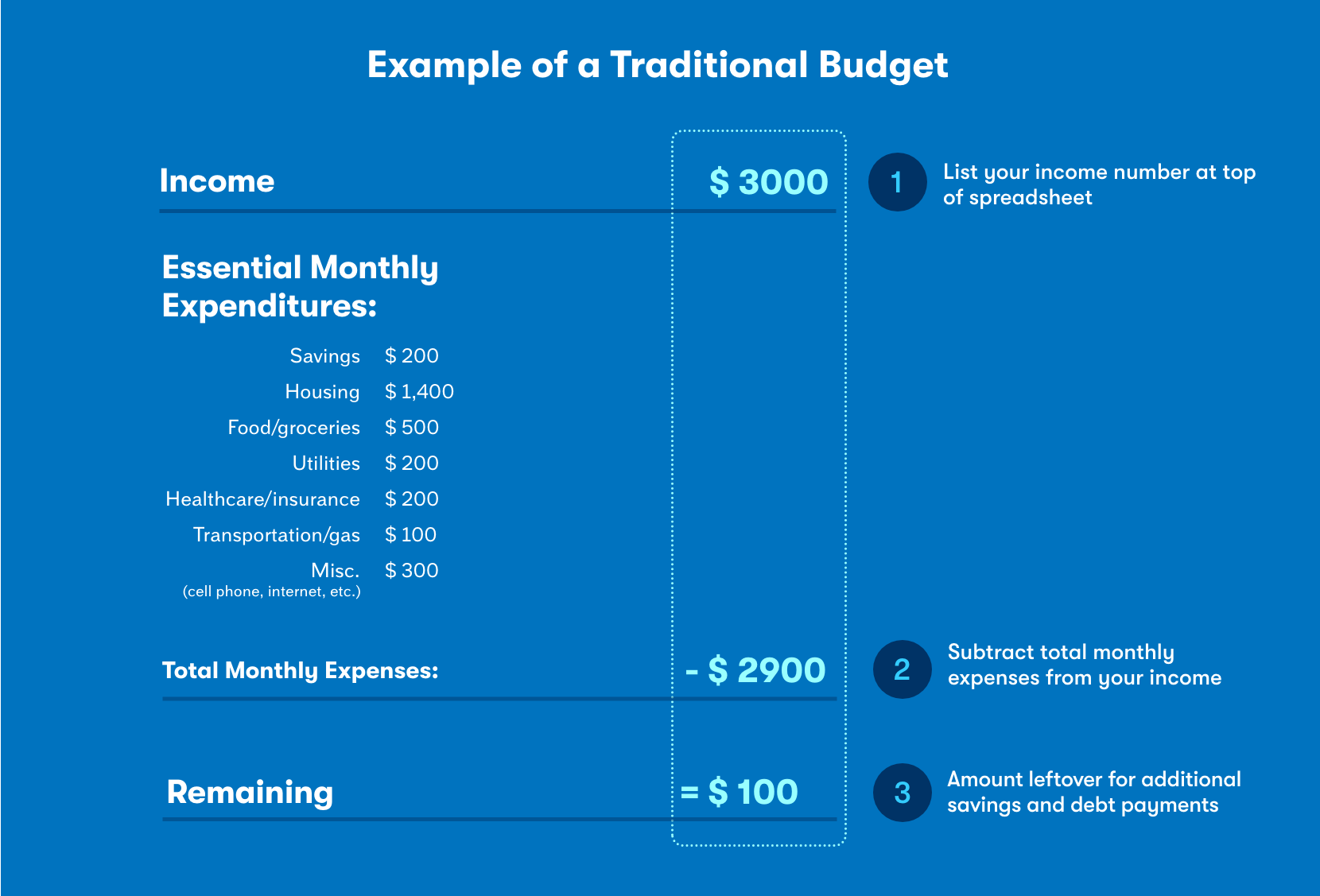

To get a feel for it, let’s create a quick sample budget. Say your take-home pay last month was $3,000. Make a simple spreadsheet that lists that number at the top, then add categories for each essential monthly expenditure. To find these amounts, you’ll want to gather all the necessary information, including last month’s bank statement and any applicable receipts.

In this scenario, your living expenses add up to $2,700. Subtract your total living expenses from your take-home pay to get the amount leftover for savings and debt payments: $300. From there, you can decide how to allocate those leftover funds.

Each month, you can add a new tab to your spreadsheet, copy over last month’s numbers, and then make any adjustments required. At the end of each year (or really anytime you wish), you can add up any category to see how much you spent or saved.

Traditional budget example:

Budgeting Pros and cons

Traditional budgets offer a proven way to save money. They help you see exactly where your money is going, so you can pinpoint areas where you may be overspending and find ways to reallocate those funds for better use. And once you know how all your money will be allocated each month, you can rest easier knowing that all your bills and expenses will be paid, no matter when they’re due.

But traditional budgets do have their drawbacks. For one thing, they can be a lot like New Year’s resolutions—you might start off extremely committed but lose interest over time. Also, budgeting typically requires an attention to detail that can easily become overwhelming. For example, you might struggle with establishing meaningful categories in your budget. Do diapers belong in the “grocery” category, or do you create a separate category for “baby”? Navigating these questions can make some people feel like giving up before they start. Traditional budgets aren’t a one-size-fits-all solution for managing money.

Another often-overlooked requirement for successful budgeting is to have a little bit of cushion in your account — savings or credit cards to fall back on if you need to bridge the gap between paying bills and payday. If your checking account spends too much time bouncing around zero, balancing your income and expenses across a month might not keep you from overdrafting your account.

If budgeting hasn’t worked for you in the past, cashflow management might be the missing strategy that will solve your issues.

What Is cash flow management?

Cash flow management is a way to track your income and expenses day-by-day. It’s also the budgeting alternative that most people have never heard of, and yet many are already doing it — particularly among the growing number of Americans who participate in the gig economy, earn an irregular income, and don’t want to (or can’t) rely on short-term borrowing solutions like credit cards.

According to a 2019 study conducted by JP Morgan called “Weathering Volatility”, “Inconsistent or unpredictable swings in families’ income and expenses make it difficult to plan spending, pay down debt, or determine how much to save. Managing these swings, or volatility, is increasingly acknowledged as an important component of American families’ financial security.” If this describes you and your family, cash flow management may be your best option.

How does cash flow management work?

The key to a successful cash flow management system is timing and expense tracking. This is because you’ll need to sync your income with your bill due dates and amounts owed in a way that ensures your success. For example, you don’t want to find yourself in a situation where your water bill is due on the 15th, but you won’t have enough money to cover it until the 20th.

The simplest way to start a cash flow management system is to write all your household pay dates and bill due dates on a calendar. Include the amounts, or your best estimates. You’ll likely see immediately where you are at risk of running out of money. Often, people find that a particular two-week period in a month is unevenly loaded with bills.

Here’s a simple example:

As you can see in the calendar above, this person is at risk of running out of money — and potentially paying an overdraft fee — before their second paycheck comes in on the 15th. By tweaking the timing of these expenses, they can avoid that fee. For example, they could do a smaller grocery shop at the beginning of the month and push the bigger shopping trip to sometime after the second monthly paycheck. Or they could try to change the due date of one of their bills. Many companies are open to this kind of request, especially if it ensures you’ll be able to pay on time.

Cash flow management pros and cons

As with traditional budgets, cash-management systems have their pros and cons. As we’ve already demonstrated, a well-thought-out cash flow system that syncs paycheck dates with bill payment dates can help you manage your expenses even when money is tight (and leaning on credit isn’t an option).

On the other hand, this kind of system can go wrong if you don’t get all your dates right. And while cash flow management can be effective at helping you work through day-to-day finances and avoid costly bank overdraft fees, it can also keep you focused on short-term issues, which may cause you to neglect longer-term planning.

However, when combined with long-term planning, cash flow management can be the tight control you need to keep your finances on track.

Which method Is best for you?

Here’s a quick recap of each method to help you determine which one might best suit your needs.

A traditional budget works well if you:

- Earn a predictable income (the same amount at the same intervals each month) and

- Have savings or credit cards you can use if necessary and

- Have a cushion available to handle expenses as they come without worrying about timing

A cash flow management plan may be needed if you:

- Earn a fluctuating income or

- Don’t have a cushion or credit cards to bridge the gap between paydays or

- Sometimes run into issues even though your income is higher than your expenses

The bottom line

Like any choice you make about your finances, selecting a money management method is highly personal. If you love a traditional budget, that’s great. If not, that’s okay too — as you can see, there are other options available. Regardless of the method you choose, the most important thing is to find an approach that helps you spend less than you make — and one that’s easy to stick to!

About the author

Jonathan Walker believes improving our personal financial resilience is about living our best lives.