Responsible Borrowing

How to Borrow Money From Friends and Family

Dec 8, 2021 16 min read

Borrowing money from family or friends is very common. In fact, research by the Consumer Financial Protection Bureau (CFPB) shows that as many as one in five people get such financial support. It’s natural to turn to those close to us whenever help is needed. After all, helping a loved one out of a financial jam can be an expression of friendship and caring. But it also can end poorly and hurt a valued relationship. The good news is there are things you can do to make sure money doesn't ruin your relationships.

How to Consider the Relationship When Borrowing Money from Family or Friends

Getting financial help from those you know and trust can have a lot of positives. Doing so, for instance, can be a more affordable, flexible and private alternative to other types of borrowing. If you're in need of money to get out of a financial emergency and you know Aunt Phyllis has enough to spare, there are a lot of good reasons to turn to her first. But in some circumstances, there are potential drawbacks to keep in mind that could strain your relationship if things don’t work out smoothly. That’s why it’s important to consider a few things first to preserve that bond.

Ask yourself these questions

When you ask a loved one to lend you money, you are asking this person to value your relationship over their money (or at least the risk of losing that money). So, consider the request from their perspective. No one wants to feel manipulated or cornered. It's important that you approach the situation respectfully. Ask yourself:

- What amount do I need and why do I need it?

- Do I have any other ways to meet this need right now, other than borrowing?

- Would there be hard feelings either way if the person I ask says no?

- If they agree, am I prepared with a plan to pay it back?

Consider who’s involved

It’s worthwhile to think about who you’re asking, too, in the context of the ability to provide financial support. Are you familiar with whether they have the means to help, or do they live on a fixed income? Would lending money to you put a strain on Uncle Stanley’s budget?

What type of financial arrangement is the best match?

Next, consider the type of framework — informal or formal — that makes sense in the context of your relationship. The loan amount may dictate the approach, but there are other factors to gauge, too.

When borrowing money, the arrangement says a lot about expectations. Formal arrangements can be used to set firm expectations. They may be most appropriate for relationships that are not close, or for situations where structure is important to maintain the respect the financial arrangement requires. Informal arrangements may be a better approach for smaller amounts of money and close relationships where a formal arrangement might feel overly prescribed.

Another consideration that is often overlooked is whether you should propose an interest rate on the loan. If no interest is charged, the transaction is a “favor” and relies heavily on the strength of the relationship. When interest is charged, the formality of the transaction will change among both parties. It may be inappropriate to tell your sister Pam that you will pay interest, just as it might be inappropriate to give an interest-free amount to your distant Uncle Michael. Interest changes the loan to a market transaction. This can be a good thing, if a formal arrangement better meets everyone's needs, but it can also subtly undermine the emotional value of the relationship and risk it becoming “all about money.”

How to Ask for Money from Family or Friends

It’s understandable to feel a little anxious or awkward when asking to borrow money. But as challenging as it can be, having a candid money conversation doesn’t have to be difficult if you have the right pieces in place. Here are some guidelines to follow once you’ve made the decision to ask to borrow from family or friends.

Have the money conversation

Choose a time to talk when you both can focus without distractions – and come fully prepared. Have a clear idea of how much you need and why; after all, if a bank asks for details, shouldn’t a family member be given the same courtesy? You should also be able to outline a sensible, well-thought-out plan for repaying the money; if you have no idea how you will pay them back, why would they believe you could?

Coming prepared to the conversation shows that you respect them, value their resources and that you take the loan seriously. Keep in mind the goal is to come up with an arrangement that works for everyone involved, so be ready to discuss questions or concerns openly. Then, don’t assume you’ll get an immediate answer. Encourage your relative or friend to think about it and get back to you when they’re ready.

Share purpose and clarify expectations

Be as upfront and honest as you can about the reason for your money need. Financial support from family and friends takes many forms, whether it’s temporarily helping with the rent after a sudden income drop or covering an unexpected medical bill.

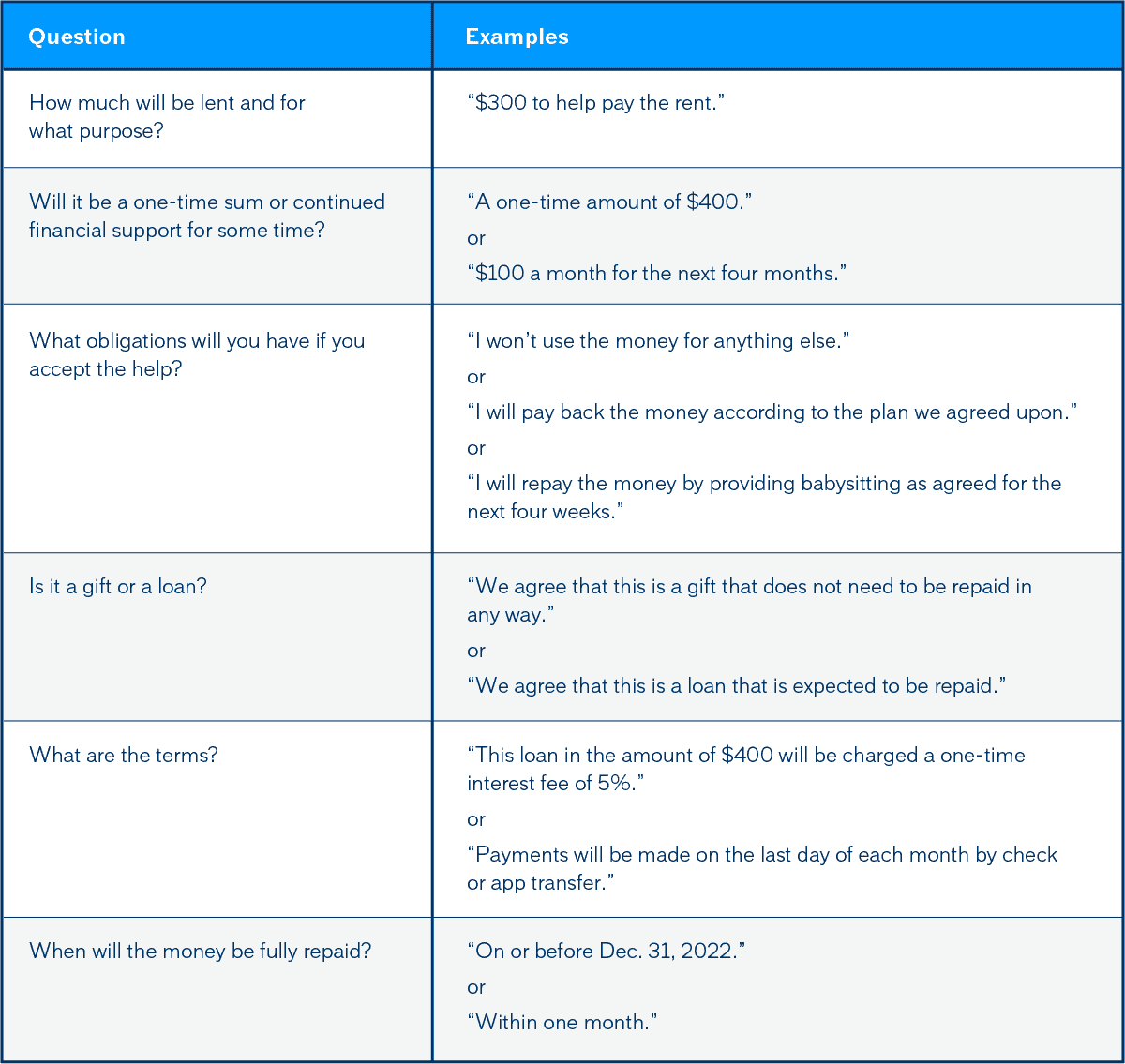

Next, discuss expectations, which could be different between the two of you. For example, here are six questions that should be answered and thoroughly understood:

Tips to Manage a Family Loan Agreement

Even with the best intentions, borrowing money from family and friends sometimes leads to strained relationships if the arrangement doesn’t work out as planned. A recent survey found that 37% of people who lent cash to relatives or friends said they lost money and 21% said their relationships were harmed. So, it’s important to remember that no amount of money is worth destroying a longtime relationship. Your aim is to do what you can to eliminate that risk. If you’ve got an informal loan from a family member or friend, here are a few things to follow through on.

Focus on follow up

If you’ve agreed to pay back the amount in installments or by a certain date, give periodic updates on where you are in your repayment plan. It’s better if you provide the occasional follow-up, so that your family or friend doesn’t have to ask about it routinely. More importantly, initiating the contact will prevent these conversations from being held when they are unwanted (like at family events or holidays). Plus, good recordkeeping means everyone’s on the same page.

Communicate as needed

Once the arrangement is made, trust it. A family loan agreement shouldn’t change everything — in particular, how you interact. You should be able to see each other, visit and spend time together without discussing the money. If you have clearly communicated and you are on track, there is no reason you have to talk about the loan every time you see them. If you make the relationship all about the loan, don't be surprised when they make the relationship all about the loan. That said, if you need to alter the plan, however, be ready to communicate openly and promptly.

Express gratitude and show responsibility

You’d likely thank anyone who did you a favor. But when it’s a relative or friend who helps you when you’re short on money, it’s essential to acknowledge what they’ve done and how much you appreciate it. What’s more, demonstrating responsibility by using and repaying the loan as agreed also goes a long way toward maintaining your relationship.

Benefits and Risks of Borrowing Money from Family

Everyone can have ups and downs with their finances. And borrowing money from family or friends is one way of balancing the low spots without resorting to other lending methods or sources of cash.

As you pursue options for borrowing, however, always consider the relationship and take steps to plan the approach with care. Whether it’s a one-time helping hand or repeated support, there are ways to borrow money from family or friends without sacrificing close-knit ties. By clarifying expectations and meeting responsibilities, you can avoid potential misunderstandings, reach a good outcome and keep your relationship strong.

About the author

Jonathan Walker believes improving our personal financial resilience is about living our best lives.