SUMMARY

- A line of credit is a flexible form of financing that allows you to withdraw cash as you need it, up to your credit limit.

- Payment amounts will vary month to month based on the outstanding balance.

IN THIS ARTICLE

- What is a Line of Credit?

- What is the Difference Between a Personal Loan and a Line of Credit?

- How Does a Line of Credit Work?

- How Can You Use a Line of Credit?

- What Are the Pros and Cons of a Line of Credit?

- How Do You Get a Line of Credit?

- Is a Line of Credit Right for You?

- Tips for Success with Your Line of Credit

Most Americans are well acquainted with loans. Maybe you have a mortgage, a car loan, a student loan or a personal loan you’re paying off.

But what about a personal line of credit?

This unique financial solution isn’t that widely known or understood. If you’re not familiar with them, you may be wondering what they are, how they work and whether this type of financing is right for your situation.

Here’s what you need to know:

What is a Line of Credit?

A line of credit is a form of revolving credit that lets you access cash on demand up to a certain limit. You can withdraw $300 today, $200 next month, and so on. Borrow only what you need — as many times as you need to — without repeatedly applying for new financing.

Unlike a personal loan, which provides a single payment up front, a personal line of credit allows you to borrow cash as needed. Keep in mind that the amount to which you have access varies depending on the terms you’re offered by your lender.

You may already be familiar with a Home Equity Line of Credit (HELOC) — the cousin to a personal line of credit. With a HELOC, you gain access to an available pool of money based on the equity you own in your home. Often, borrowers use a HELOC to finance major purchases, like a home renovation.

Unlike a HELOC, a personal line of credit is typically unsecured — meaning it doesn’t use your home (or any property) as collateral. People generally tap a personal line of credit for relatively small expenses of a few hundred to several thousand dollars.

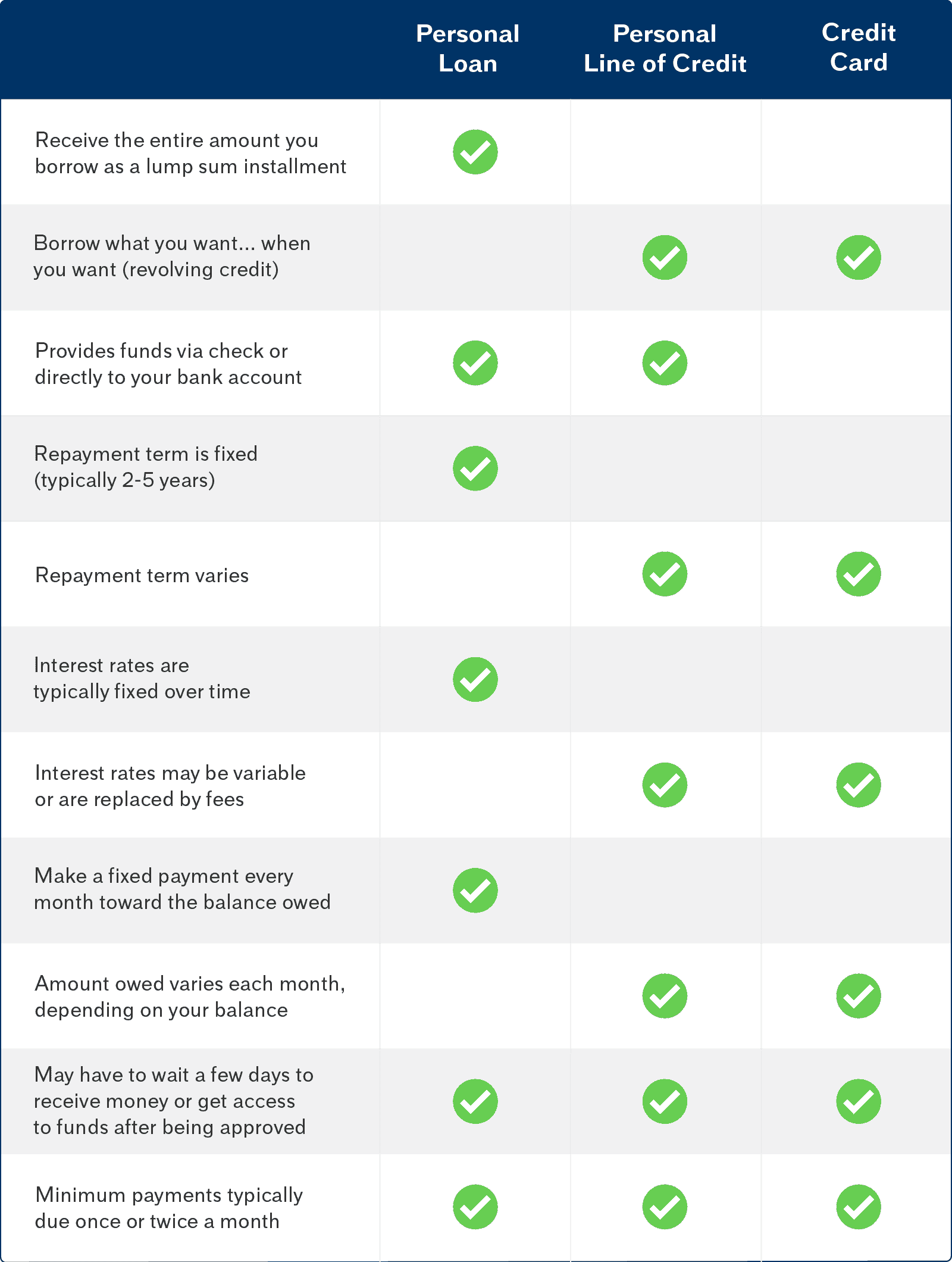

What is the Difference Between a Personal Loan and a Line of Credit?

A personal line of credit is, in many ways, a cross between a personal loan and a credit card:

How Does a Line of Credit Work?

Once you’ve been approved for a line of credit, you can request a cash advance (sometimes called a draw) when you need it — typically through an online form. After submitting your request, you may need to wait a few business days before you receive the funds. In many cases, the lender will deposit the cash in your bank account, but some may also offer the option of sending you a check.

Each month you have an outstanding balance, you’ll need to pay at least the minimum owed, as specified by your lender. As you repay the funds, you replenish your line of credit and give yourself more borrowing power for the future. And, as your balance decreases, the amount you owe each month will typically decrease as well.

What Costs Are Involved with a Line of Credit?

Fee structures vary from one lender to another. Knowing all the potential costs up front can help you evaluate if a line of credit is right for your situation.

For example, some lenders charge an interest rate based on the amount of outstanding debt. Others may charge a fee on the balance each billing cycle — typically every two or four weeks. And there may be other fees to factor in, such as origination fees, cash advance fees, annual fees, or late fees.

As you might imagine, these fees can add up — especially over time. To minimize cost, borrow only the amount you need and try to pay it back as quickly as you can.

How Can You Use a Line of Credit?

If you have variable income, a line of credit can be a great tool for smoothing out your finances if, for example, you don’t have enough money in savings. In months that you need a little extra cash, you can turn to your line of credit. And, when your income increases, you can repay your line of credit and live off your take-home pay.

But a line of credit is frequently used in other ways as well. When people anticipate multiple future costs — particularly those of an unknown size — they sometimes turn to a line of credit. For instance, borrowers may use a credit line to pay for unexpected medical bills, necessary home repairs, and even wedding costs.

What Are the Pros and Cons of a Line of Credit?

A line of credit offers unique benefits and potential drawbacks that are important to know about.

Pros:

- Flexibility. Never borrow more money than you need and only pay interest or fees on the amount you borrow.

- Debt management. It can act as a safety net in case something comes up, so you can be more aggressive with putting extra money against your debts.

- Payments may go down. Your payments will shrink as you pay off your balance, easing your monthly finances over time.

- Reported to credit bureaus. Keeping your balance small or at zero over time may reflect positively on your credit report.

Cons:

- Temptation. If it’s tough for you to avoid spending up to your credit limit, you may not want the temptation of a line of credit.

- Variable payments. It can be challenging to predict and budget for payments if your payments change regularly.

- Reported to credit bureaus. Maintaining a continually high balance on your line of credit could negatively affect your credit score.

How Do You Get a Line of Credit?

Not all banks, credit unions and online lenders offer personal lines of credit, so you may want to start with an online search to see what’s available. You can also check with your current bank or credit union to see if they offer a line of credit.

If you’re searching for a line of credit online, you’ll want to do a little research to make sure the lender is reputable. Check to see if the lender has any reviews or star ratings, for example, through Google. The lender’s site should also list a physical address and phone numbers. Most will also provide information about who licensed them to lend.

When you’ve decided on a lender, the next step is to apply for a line of credit. The lender will review your credit report, determine whether you meet their lending criteria, and — if you do — offer you specific financing terms. Those will include the total amount you can borrow from your line of credit as well as details about the cost of borrowing. Once you accept the terms and fill out the necessary forms, you’re all set to borrow cash as needed up to the credit line’s specified cap.

Is a Line of Credit Right for You?

Before you apply for a line of credit, ask yourself these questions:

- Does a line of credit fit your financing needs? If you need to borrow a one-time lump sum, consider a loan instead.

- What’s the most you’ll need to borrow at one time? You’ll want the line of credit to cover at least that amount.

- What’s the cost of borrowing the money? Effectively, how much money — beyond what you borrow — will it take to repay the line of credit?

- Can you afford the payments? If you max out the line of credit, what will your minimum required payment be for that month? Ensure that it fits your budget.

Tips for Success with Your Line of Credit

If you go with a line of credit, follow these strategies to get the most benefits from your financing:

- Stay on top of your payment schedule. Your payment history is likely reported to credit bureaus. To maximize your credit score, pay at least the minimum amount owed by the specified due dates.

- Pay more than the minimum owed, if possible. Paying extra not only slashes your outstanding balance but can also reduce the interest and fees you owe — as well as the length of time you’ll be in debt.

- Keep your balance as low as possible. Just as with a credit card, your credit score can take a dip if you use too much of your available credit. Pay off the debt completely when you can. The value of a line of credit is you can borrow again if needed, without the need to apply again. Utilization directly affects your credit score, so any little bit you can lower it would be a positive effect on your score.

Bottom Line

There’s no one-size-fits-all solution when it comes to financing, but understanding how a line of credit works can help you decide what financing will work best for your needs.

About the author

Nathan Foley questions everything — and thinks you should too. As Elevate’s resident mathematician, he pores over datasets to find the truth amid the fluff and translates insights into ideas for improving personal financial resilience.